- Joined

- Jul 25, 2008

- Messages

- 15,293

- Points

- 113

Top brass of Japanese syndicate accused of laundering $628.7m for criminals lived in S’pore

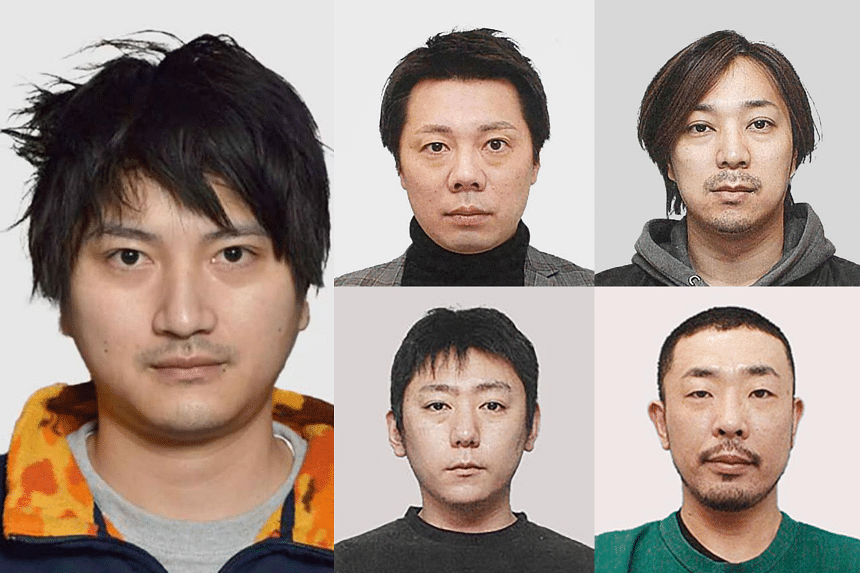

(Clockwise from left) Sotaro Ishikawa, Kosuke Yamada, Takamasa Ikeda, Hiroyuki Kawasaki and Shinya Ito. PHOTOS: OSAKA PREFECTURAL POLICE

David Sun

Crime Correspondent

Sep 20, 2024

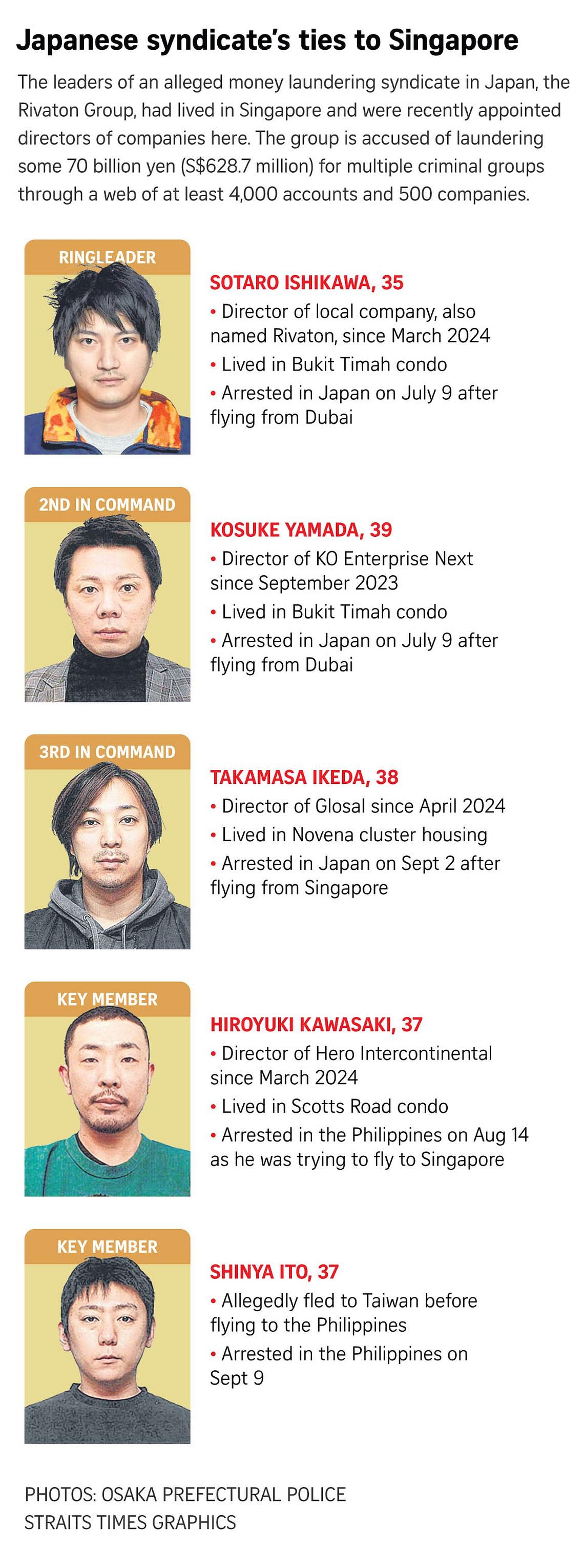

SINGAPORE - The head of a syndicate in Japan accused of laundering some 70 billion yen (S$628.7 million) for criminals there had a home in Singapore and was appointed director of a software firm here, The Straits Times has found.

Sotaro Ishikawa, who fled Japan in February amid an investigation by the police, led the Rivaton Group.

The criminal syndicate is believed to comprise more than 40 people.

The 35-year-old lived in a condominium in Bukit Timah, and was registered as the director of a local software company, also named Rivaton, in March.

Checks by ST showed that a number of others in the syndicate were also appointed directors of companies in Singapore over the last two years.

Rivaton’s second in command, Kosuke Yamada, was appointed director of local software company KO Enterprise Next in September 2023.

The 39-year-old, who goes by Yamada Kosuke here, also has a registered address in Singapore at the same condo as Ishikawa.

Both men told the Japanese authorities they were Singapore residents when they were arrested on July 9, after flying back to Japan from Dubai, reported Japanese news agency Jiji Press.

The third-ranking officer of the group – Takamasa Ikeda, 38 – was arrested on Sept 2 at Kansai International Airport after taking a flight from Singapore to Japan.

Ikeda has a registered address in Singapore at a landed property in Novena. He became the director of local advertising company Glosal in April.

According to the Osaka Prefectural Police, the group had systematically set up shell companies in Japan from 2021, and used the corporate accounts of these companies to launder criminal funds linked to scams and illegal gambling.

At least 4,000 accounts and 500 companies involved in the scheme have been uncovered by the Japanese authorities so far.

On May 21, the police arrested 12 people linked to the group in Toyama, Japan.

The authorities in Japan released a wanted notice in August with the names and pictures of the five alleged leaders of the group who reportedly left the country between January and April.

They include Ishikawa, Ikeda and Yamada.

Two others were arrested in the Philippines, including Hiroyuki Kawasaki, 37.

He was about to board a flight to Singapore on Aug 14 when he was arrested at the Ninoy Aquino International Airport in Manila by the Philippine authorities, reported NHK.

Business records show he became the director of local consultancy firm Hero Intercontinental in March.

The fifth wanted man – Shinya Ito, 37 – had initially fled to Taiwan before flying to the Philippines to hide. He was arrested there on Sept 9.

The Philippines does not currently have an extradition treaty with Japan, but Japanese news outlets have reported that both Kawasaki and Ito are expected to be sent back and handed over to the Japanese authorities in due course.

Checks by ST found that Ishikawa, Ikeda, Yamada and Kawasaki still have valid employment passes here.

Singapore PR

The Singapore companies linked to the wanted men were all set up by a lawyer who is a Japanese citizen and a Singapore permanent resident.He is registered with the Accounting and Corporate Regulatory Authority as a corporate service provider.

He said he set up the companies on the instructions of lawyers at two different firms, and added that he had performed due diligence checks on the Japanese men and their purported business dealings.

“Even though (the law firms) had conducted their own checks to meet the regulatory requirements, I met the suspects via Zoom as well as in person in Japan for verification purposes, and I visited their office in Japan for further verifications and due diligence and to witness their passports,” he said.

“After the whole $3 billion money laundering case in Singapore, I was extra careful. But there was nothing that appeared to be suspicious.”

He said that he questioned the men about their source of wealth and why they wanted to set up companies here.

The men told him the money was from the Rivaton Group, which at the time appeared to be a legitimate business, and that they wanted to set up the companies here for tax purposes.

He said that, as a lawyer, he knew the importance of conducting thorough checks to prevent money laundering.

His checks showed that the men lived in rented properties in Singapore and did not appear to own luxury vehicles.

They relied on public transport instead.

He said that he flew to Japan twice to check their identities and office premises, and found the business set-up to be normal.

The lawyer said he last met the men in April.

Japanese daily Sankei Shimbun reported that the Rivaton Group, which claims to be a payment solutions provider, had allegedly laundered funds for multiple criminal groups.

A senior police official was quoted saying the Rivaton Group operated just like a normal company, with members typically working office hours, attending meetings and being paid a salary.

The company had a handbook on how to answer questions from auditors and financial institutions to avoid suspicion.

The syndicate has been accused of using a system that automatically transferred funds from one bank account to another, with transfers triggered by either account balances or time passed.

Ishikawa, Yamada and Ikeda were the top brass, while a layer of executives split into different departments reported to them.

These departments included one that managed the automated system, another that oversaw transfers, and another that handled the opening of accounts and responding to queries from financial institutions.

A third tier of low-level collaborators was recruited through social networking sites to set up the shell companies.

The group also set up bases in Tokyo and Toyama, so it could still operate in the event of a system outage.

The lawyer in Singapore said he was shocked when he recognised one of the men arrested in the probe in Japan.

He immediately filed a suspicious transaction report here and contacted the Japanese police with information.

Shortly after, he flew to Japan to provide more details on the possible whereabouts of the wanted men, who were later arrested.

The lawyer said he has not been contacted by the Singapore authorities in relation to his suspicious transaction report or the case involving the Rivaton Group, but added that he has been cooperating with the Japanese authorities.

He said: “I want the Singapore authorities to contact me, actually, so that they’ll know I did my best and there was nothing else I could do.”

Wu Duanren and Zhang Jie, two men who are said to be linked to online casinos in the Philippines and who allegedly helped to facilitate Philippines ex-mayor Alice Guo's escape.Credit: Presidential Anti-Organised Crime Commission")