Some young investors get burnt by cryptocurrency crash, regret recklessness; experts raise depression fears

Kanchanara/Unsplash

- One investor, Mr Low, lost about S$40,000 in the crash in just days, about 90 per cent of his total investment and a third of his savings

- The crash involving stablecoin Luna has led to concerns about suicide ideation and reckless behaviour

- One enraged investor, who reportedly lost US$2.3 million in the crash, tried to break into the Seoul home of a businessman involved in the technology behind the cryptocurrency

- Holding funds in a related token, TerraUSD, was particularly popular among some Singaporeans

- Some platforms that allow users to deposit and borrow cryptocurrencies were offering an interest rate of about 20 per cent a year for deposits of TerraUSD

BY

DARYL CHOO

BY

KIMBERLY LIM

Published May 17, 2022

SINGAPORE — He was just having his breakfast when he opened up his cryptocurrency exchange application and was shocked to see his Luna tokens at US$5.28 (S$7.35) and spiralling downwards last Thursday morning (May 12). In early May, the tokens were trading above US$85 apiece.

Confused, the man, who wanted to be known only as Mr Low, immediately messaged friends who had invested in Terra, a related cryptocurrency, hoping to find out what was happening.

He said: "A few friends told me that it will repeg (to the US dollar) and Luna will stabilise, so I just held."

Mr Low, who is in his late twenties, had recently lost his job as a business associate at a consumer health company due to company cutbacks, and said that he had lost close to S$40,000. This was 90 per cent of his total investment and a third of his savings in a matter of days.

He said: "Initially, it was a lot of confusion. I was not aware, unlike now, of why the market was reacting that way and why UST (TerraUSD) had depegged (from the US dollar) and Luna was spiralling. There was some blind hope that it would repeg, so I just kept holding and not selling."

Over the past week, the cryptocurrency market went into a

full meltdown after investors were spooked by the collapse of TerraUSD, or UST, one of the world’s largest so-called stablecoins.

Stablecoins are digital tokens pegged to the value of traditional assets, such as the US dollar. Often promoted as a stable means of exchange, these coins are often used by traders to move funds around when speculating on other cryptocurrencies.

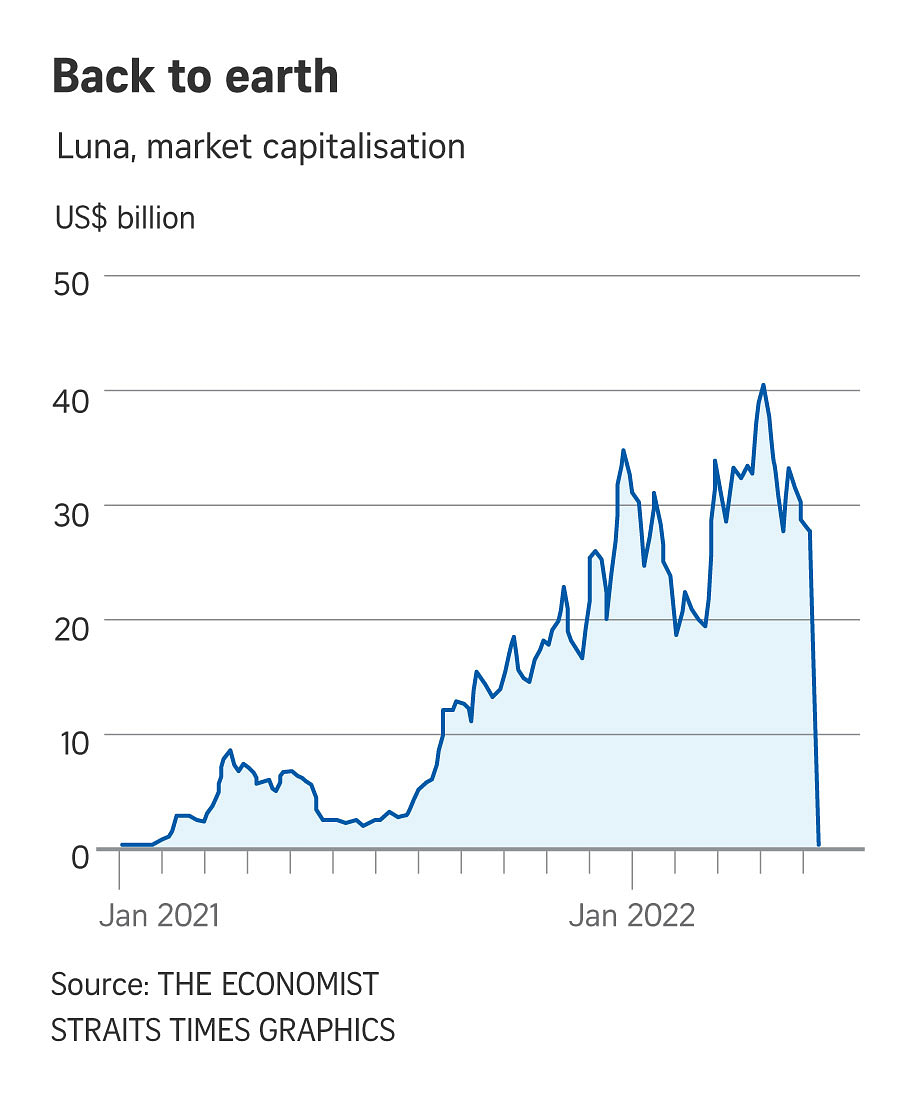

Last Tuesday, TerraUSD broke its 1:1 peg to the US dollar and fell as low as 75 US cents, according to price site CoinGecko. Its price is now hovering around just nine US cents.

Unlike other stablecoins that have reserves in traditional assets, TerraUSD maintains its peg through a complex algorithm that involves the use of another cryptocurrency token, Luna.

Luna, once ranked among the top 10 most valuable cryptocurrencies, has since plunged to virtually zero from an all time high of US$119.18 set on April 5 this year.

Luna and TerraUSD are tokens that run on the Terra network, a blockchain-based project developed by start-up Terraform Labs, that is based in Singapore.

The crash had led to concerns about suicide ideation and reckless behaviour, with one enraged investor, who had reportedly lost US$2.3 million in the crash, attempting to break into the home in the South Korean capital Seoul of Terraform Labs’ co-founder and chief executive officer, Do Kwon on Monday.

In a series of tweets on Saturday, Mr Do wrote that he feels “heartbroken about the pain” caused by the crash, adding that he has not profited from this incident and has not sold any TerraUSD tokens during the crisis.

The stability of such cryptocoins was once the cornerstone of the crypto ecosystem, with the United States Federal Reserve estimating a collective market value of all stablecoins at US$180 billion in March this year.

“

Mentally I am okay, my faith reminds me that life is bigger than a financial portfolio, and though I was irresponsible in risk management, I would accept the mistake and move on and not harp on it.

Cryptocurrency investor Mr Low, who lost about S$40,000 in the crash

”

TODAY spoke to seven Singaporeans, aged in their 20s and 30s, whose investments in TerraUSD and Luna, ranging from S$1,500 to S$6,000, took a tumble last week.

While some were aware of the risks involved in cryptocurrencies and were sceptical when they entered the market, others had a larger risk appetite or believed that it was "risk-free".

Holding funds in TerraUSD was particularly popular among some Singaporeans, as some platforms that allow users to deposit and borrow cryptocurrencies were offering an interest rate of about 20 per cent a year for depositing TerraUSD on their platform.

And these holdings were “risk-free” because the TerraUSD tokens are pegged to the US dollar and would not lose their value, or so the investors thought.

Mr Low said that he had friends who were invested in the Terra ecosystem.

"At the time, this meant you unlocked a savings rate that beat the Singapore banks by 400 times on an annual basis. And that it was 'risk free' so lots of people jumped onto the boat. They are coping just fine as a majority of their losses are purely paper profits," he said.

Another investor, who wanted to be known only as Ashton, 37, who works as a technician, said that he lost about S$6,000 from the crash, but his portfolio was still mainly in other coins such as bitcoin and ether.

LUNA CRASH HAS RAISED CONCERNS ABOUT SUICIDE IDEATION

However, many others saw their life savings wiped clean over the span of two days, prompting suicidal thoughts in some of them. Some personal finance writers have raised concerns about suicide ideation following the crash of Luna.

At least one member of a Telegram group chat centred around the local Chain Debrief cryptocurrency online publication have spoken about attempting suicide, which has been a “cause for concern” for Mr Jacky Yap, the publication’s founder.

He told TODAY in an interview last Friday: “We remind everyone to not do anything foolish, and if anyone needs to talk to someone, they can always reach out to us. We also remind everyone that we all have earning power and that whatever is lost can always be earned back.”

Indeed, this is a trend happening in other parts of the world, with moderators of the Reddit threads on Terra and Luna pinning a post with suicide hotline numbers, over concerns voiced in the thread.

The Woke Salaryman, a page on personal finance, with more than 316,000 followers on Instagram and almost the same number of likes on Facebook, posted a series of graphics on Tuesday reassuring people who lost money to the crash.

The graphics were captioned: “ We typically don't like to post three times a week. But this is important”.

The post on Facebook had garnered more than 10,000 shares and 8,900 reactions five days after it was posted. The co-founders behind the page also received several direct messages on social media platforms, with fellow investors airing their grievances.

Speaking to TODAY in a Zoom interview last Friday, Woke Salaryman co-founder He Ruiming said: “Quite a few people sent direct messages to us. We are in quite a few crypto groups as well so I see quite a lot of people talking about being depressed, saying that everything is hopeless now. So we thought it would be important to put out a message.

“People came to confide because they knew I invested as well. They asked me: ‘What should I do?’ By the time the news came out, there was already very little people could do.”

YOUNG INVESTORS TRYING TO MOVE ON

Some were “mentally prepared” for the crash, while others are looking for ways to move on.

Mr Low said: “Mentally I am okay, my faith reminds me that life is bigger than a financial portfolio, and though I was irresponsible in risk management, I would accept the mistake and move on and not harp on it.”

Personal finance writers and bloggers are urging young investors to try to find ways to recover from the crash.

Mr Timothy Ho, managing editor and co-founder of investing website Dollars and Sense, said: “If you are young, it’s not the end of the world. Maybe you lost money that could have paid for one to two holidays to Europe which you didn’t get to go due to the pandemic, or the down payment to a car. It’s okay to move on.”

Many emphasised the importance of having a diversified portfolio, which should be a key takeaway from the crash.

“Having a diversified portfolio is vital because if you lose a huge chunk of your portfolio at once, it’s hard to recover. A diversified portfolio may not give us the highest possible returns, but will protect us in bad times like this,” Mr Ho said.