Like many other property developers, Country Garden’s business took off in 2015, when many cities started urban redevelopment projects, becoming the largest developer by sales in 2017.

Before regulators tightened controls on their financing in 2020, Country Garden thrived on borrowed money. Relying on high leverage, rapid turnover and massive borrowing, the company expanded quickly in China’s small and medium-sized cities.

But the crackdown on financing aimed at curbing risks at overleveraged developers put an end to that growth model.

Compared with many of its distressed peers, Country Garden was in a better position during the early stages of the property market downturn as it managed to repay debts, deliver projects, and make use of government support to borrow money from financial institutions and issue bonds. However, the deepening market decline since mid-2021 has amplified the company’s capital challenges.

Now, Country Garden is scrambling for a lifeline. The company is mulling over restructuring its onshore bonds and has hired China International Capital Corp. Ltd. as a financial adviser, sources with knowledge of the matter told Caixin.

As the company is short of cash to make repayments for its maturing onshore bonds or those with a put option due in September, it may first extend those before dealing with offshore bonds, according to the sources. Relieving some of the immediate repayment pressure could help it focus on completing presold housing projects, they said.

Country Garden last week proposed extending an onshore bond maturing in September by three years, but faced challenges in securing approval from bondholders. On Friday, the company made a last-minute change to postpone the deadline for holders to vote on its debt extension plan in the latest effort to avert a default.

“If no external force comes to its rescue and Country Garden falls apart, other private property developers will collapse one by one, and the last bit of market confidence will be worn away,” an executive at a bond investment company said

Sliding into crisis

By the end of 2022, Country Garden’s financials appeared fairly sound. The company had 147.6 billion yuan in available cash on its balance sheet, including unrestricted cash and cash equivalents amounting to 128.3 billion yuan — sufficient to cover its short-term debt of 93.7 billion yuan due in 2023.

However, the company recently told creditors that its available funds are only enough to complete existing projects, without giving any explanation of its worsening liquidity, a bondholder said.

Country Garden is known for its strategy of tightly controlling spending based on revenue. Land acquisition and construction costs usually constitute the major portion of a developer’s expenditures.

As the market cooled and sales slowed, Country Garden’s spending on land purchases slid to 5.8 billion yuan in the first seven months, ranking the 24th in the industry, according to independent real estate research institution China Index Academy.

But the company’s spending on construction has remained high as it strives to deliver projects on schedule under pressure from authorities. Last year, discontent over long stalled projects triggered protests and mortgage boycotts in many cities, forcing local governments to step in and urge developers to complete construction on time.

In 2022, Country Garden delivered housing 700,000 units, the most among all developers and exceeding the combined amount completed by China Vanke and Evergrande, according to Caixin’s calculation based on public information. Country Garden said it expects total 2023 deliveries to reach another 700,000 units, with its first half deliveries totaling 278,000.

But compared with Vanke and Evergrande, which focus more on big cities, Country Garden’s heavy bet on third- and fourth-tier cities means its promise of housing deliveries could be much pricier as housing sales and prices have plunged deeper in smaller cities.

“Consider a project with 500 units. If only 100 units were pre-sold, the entire project must be completed to ensure the delivery of these 100 units, regardless of when the remaining 400 units can be sold,” a real estate company staffer said. The greater the number of units that are sold in advance and at higher prices, the lesser the funds developers need upfront to cover construction costs, said the person.

S&P Global estimated that Country Garden’s 2023 construction costs will be around 130 billion yuan.

Based on Country Garden’s 2022 financial data, the company needs monthly sales of at least 22 billion yuan to keep construction on schedule and maintain basic operations, excluding debt payments and land purchases, according to a banking industry insider.

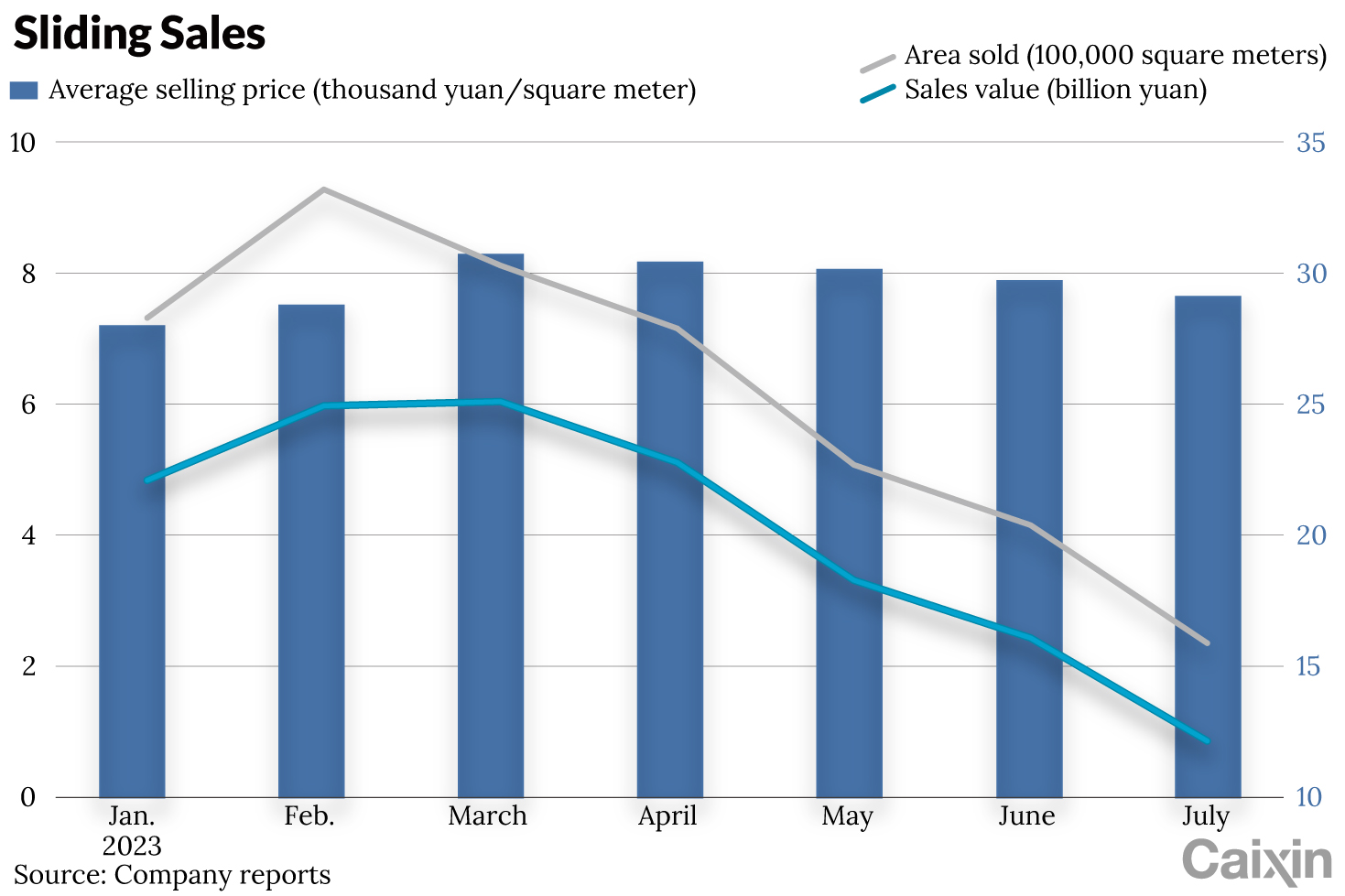

But Country Garden’s sales have been sliding this year. In the first seven months, they fell 35% year-on-year to 140.8 billion yuan, according to the company. This exceeds the industry’s average drop of 4.7%during the period, according to data China Real Estate Information Corp. (CRIC).

Although Country Garden maintained its top position in terms of area sold, it slid to sixth place in terms of sales value, CRIC data showed. That underscores the company’s business weakness due to its focus on smaller cities, which experienced faster growth over past years, but were also hit much harder in the latest housing market downturn.

Amid weakening demand, housing inventories in third-and fourth-tier cities reached 19 months of supply in May 2023, compared with 12.3 months in the top-tier cities, according to CRIC.

In a recent letter to investors, Country Garden’s management apologized for its recent troubles and for the first time acknowledged the company’s overreliance on smaller cities, saying its awareness of potential risks was inadequate.

Capital drain

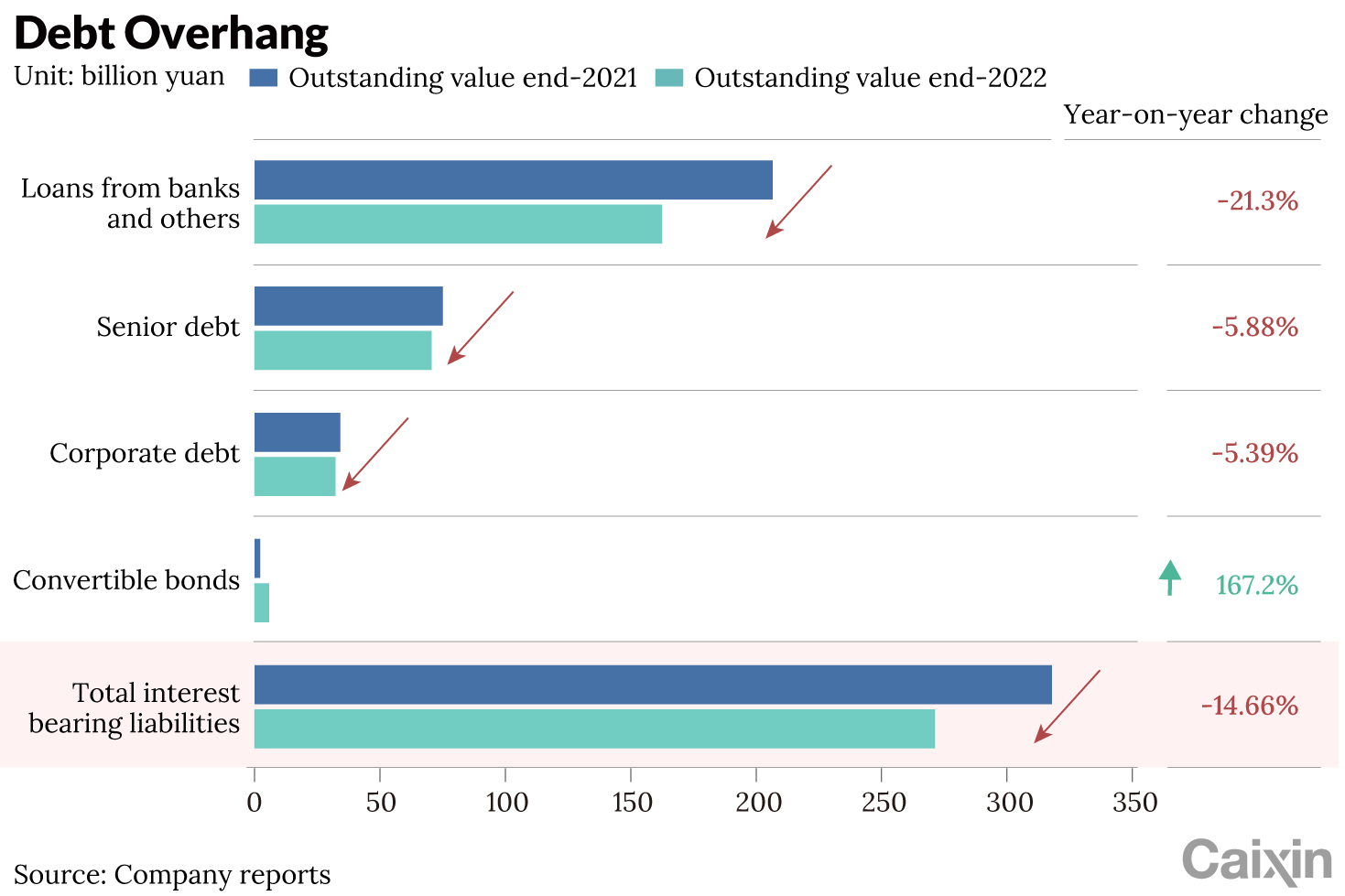

At the end of 2022, Country Garden’s interest-bearing liabilities totaled 271.3 billion yuan, a decrease of 98.3 billion yuan or 26.6% from 369.6 billion yuan in 2019, according to the company’s financial report.

Country Garden’s efforts to reduce its debt burden are evident, but the sheer magnitude of the problem remains a significant challenge and has greater financing demands, several financial institution sources said.

“The current financing environment for private enterprises is undeniably harsh,” said a banking source familiar with the company.

Country Garden had maintained a positive cash flow from financing for 13 consecutive years before 2019, company financial reports showed. But it did an abrupt about face in 2020 after authorities laid out “three red lines” that set leverage benchmarks builders had to meet if they wanted to borrow more money. From 2020 to 2022, the company posted an accumulative net outflow of 125.7 billion yuan.

Bank loans were an important source of funding for Country Garden. In 2022, its borrowing from banks and other institutions totaled 162.5 billion yuan, down 44 billion yuan from the previous year.

“In the second half of 2022, Country Garden had trouble repaying loans,” said a Guangdong financial industry source. “Local governments intervened to arrange loan extensions with banks, but new lending has remained limited.”

In November, a 16-point policy package to direct more financial support to the ailing property market was unveiled by the government. But industry sources said the effects have been limited, especially for private developers.

“While many private developers obtained significant preliminary credit approvals, companies that actually received loan disbursements are scarce,” said a property industry researcher at a brokerage firm.

Property projects in smaller cities in particular are given a wide berth by banks due to concerns about weak sales, said a bank executive. Another banker at a state-owned lender said government-backed developers are much more favored than their private counterparts when it comes to bank loan approvals.

Financial institutions have significantly lost confidence in private developers, and Country Garden is no exception, a person close to the central bank said.

Borrowing from the bond market is also challenging for private developers. In the first seven months, bond financing by the real estate sector totaled 285.6 billion yuan, of which only 16.5 billion yuan was raised by private developers, according to China Index Academy.

The small scale of bond issuances by private developers is not due to any regulatory restrictions, but rather because there is no demand for them, a bond regulatory official said.

Prior to its current predicament, Country Garden had better access to funding compared with most private developers as it was still able to take out loans and issue bonds with a government-backed guarantee.

Indeed, in 2022 Country Garden raised over 9 billion yuan through 10 bond issuances, according to Caixin’s calculations based on public information. But so far in 2023, the company has issued only two medium-term notes in domestic market to raise 1.7 billion yuan and an offshore note of 1 billion Thai baht ($28.5 million).

But the money raised is just a drop in the bucket compared with Country Garden’s debt obligations.

“The 1.7-billion-yuan financing is not even enough for Country Garden to cover two weeks’ expenses,” a banking industry source said.

Between delivering presold housing projects and making debt repayments, the holes in its cash flow have become too big to fill, Zhu Wence, an independent property market analyst, wrote earlier this month.

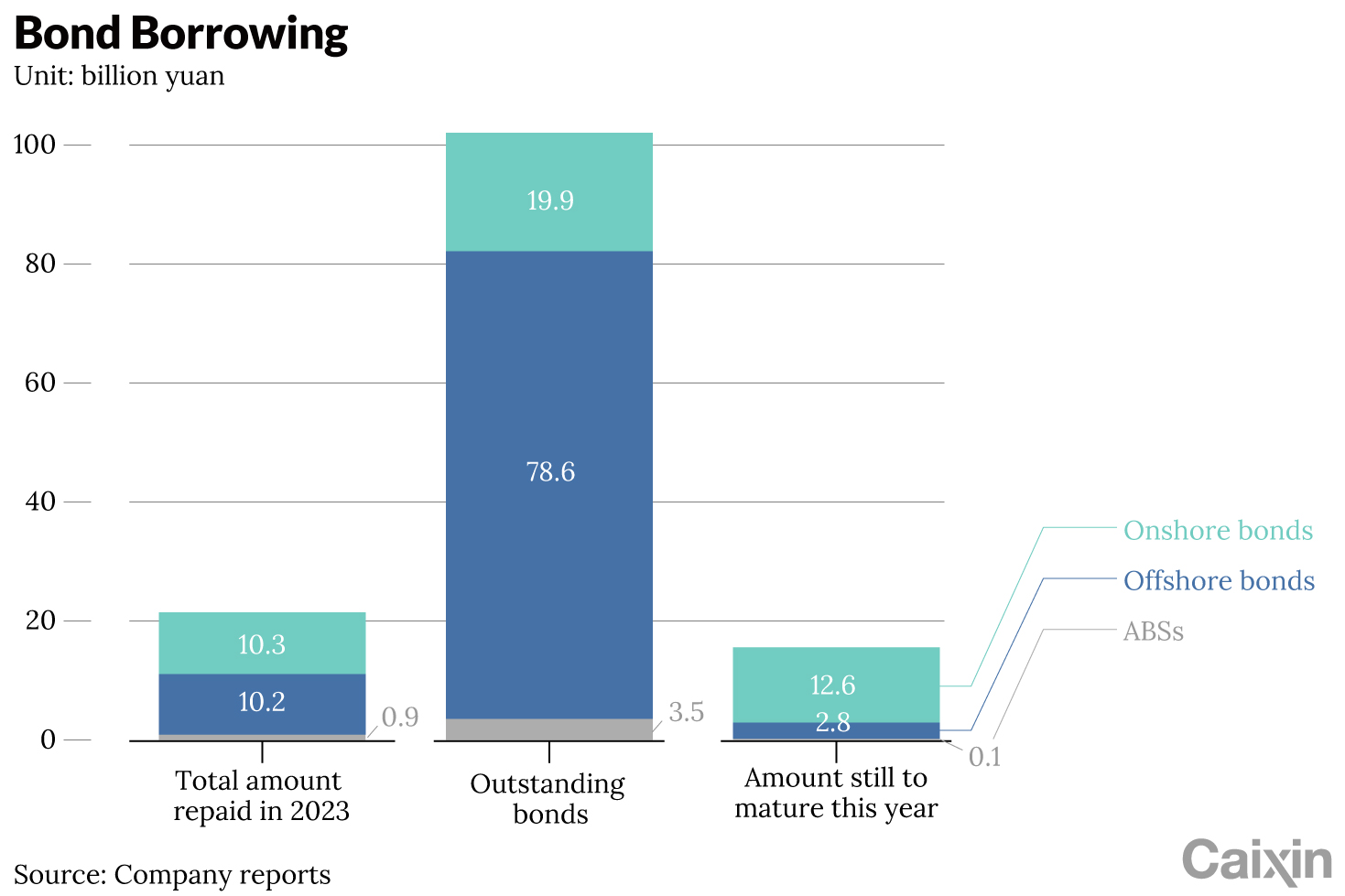

So far this year, Country Garden has repaid 21.4 billion yuan of its bonds. As of Aug. 15, the company had outstanding bonds including asset-backed securities totaling some 102 billion yuan, with 19.9 billion yuan of onshore bonds and 78.6 billion yuan of offshore bonds, according to Ratingdog. About 15.5 billion yuan of the debts will mature by the end of 2023.

Share

Share

Forest City is a large property development on four man-made islands spanning 30 sq km in the Straits of Johor. (AFP pic)

Forest City is a large property development on four man-made islands spanning 30 sq km in the Straits of Johor. (AFP pic)