Its balance is roughly only 23.5billion……you heard it first here on sammyboy.

-

IP addresses are NOT logged in this forum so there's no point asking. Please note that this forum is full of homophobes, racists, lunatics, schizophrenics & absolute nut jobs with a smattering of geniuses, Chinese chauvinists, Moderate Muslims and last but not least a couple of "know-it-alls" constantly sprouting their dubious wisdom. If you believe that content generated by unsavory characters might cause you offense PLEASE LEAVE NOW! Sammyboy Admin and Staff are not responsible for your hurt feelings should you choose to read any of the content here. The OTHER forum is HERE so please stop asking.

You are using an out of date browser. It may not display this or other websites correctly.

You should upgrade or use an alternative browser.

You should upgrade or use an alternative browser.

According to an insider, the CPF does not have enough funds to disburse to everyone

- Thread starter Satanic verses

- Start date

That's because gonmen borrowed most of that money and give 2% in return.

Oh well we will never know as the whole country won't turn 55 on the same day...on another note do we have trust in Lawrence?

CPF contract is like long-term deposit.It a thing call confidence with the system that will make people not to ask for the money back

Like someone once describes it.

At first nothing happens. Then suddenly everything happens.

Good luck to idiots who keep voting PAP. You will lose your pants eventually.

Migrate and save your children.

At first nothing happens. Then suddenly everything happens.

Good luck to idiots who keep voting PAP. You will lose your pants eventually.

Migrate and save your children.

Its balance is roughly only 23.5billion……you heard it first here on sammyboy.

Economies are based upon market confidence, as well as pragmatic policies to obtain revenues for a nation's social expenditure/budget.

Thus, if ANYONE whom claims to be in the know of such movements, such is INSIDER information - which may be TRUE or FALSE, as such a person's claim WOULD NOT BE VERIFIABLE as it is done in anonymity, & worse would be that the naive who believes such unsubstantiated claims & makes BAD judgements based upon such unvalidated data, or be made used by others with hidden corrosive agendas.,..A criminal offense amounting to TREASON.

So, do not be a complicit in treasonous activities. It is not worth it as it carries capital punishment, UNLESS that person whom initiated such rumours comes forward & present verified data & information.

So far, no citizen has been rejected for any eligible withdrawals. Thus the rumour is FALSE.

a)Singapore's GDP is $397 Billion growing annually.

b)It's tax revenue amounted to $68 Billion, financial year 2023, & spends only a needed & substantial amount of 75% of it for social expenditure -est $51 Billion - with $17 Billion in savings, which increases every year. With just simple calculations, that amount would grow to $170 billion in just a mere 10 yrs. Singapore has lasted more than 50 yrs already. So do the maths on how much is in the treasury from tax revenues alone, which DOES NOT include CPF contributions...

c)Only est 717.000 of citizens are aged 65 & above in 2023, eligible for CPF withdrawals, out of 3.5 Million working adults including foreigners, of which whom are contributing to CPF monthly.

Do your own homework, so as not be fooled or misused by others....

Expected,cos papigs use it yo invest n due greed n also economic didn't favour all lost, same as all investor, just that dumb 60% sinkies still belive,lol

Paigs I'm big shit that's,why need lots of monies

Bank retrenchment is good cos they need to reset all systems

Why do you think the PAP government is always asking Sinkies to put more money into their CPF accounts?

On this count, this is similar to a Ponzi scheme: asking Sinkies for more money so that those who want to withdraw will be paid.

CPF Life is a far cheaper and better annuity than private annuities because its return is much higher dollar for dollar, more stable and will pay you for life. ZAOBAO FILE PHOTO

Tan Ooi Boon

Invest Editor

NOV 12, 2023

Retirement planning for many people here just got a boost, thanks to some participants of the Forward Singapore dialogues who shared their views on the importance of having continuous and stable income in old age.

Their input has prompted the Government to look at tweaking the voluntary component of the CPF Life annuity scheme to allow members to increase their savings in readiness for their golden years.

As it stands now, when members reach 55, the full retirement sum ($198,800 this year) will be moved from their CPF accounts to their Retirement Account (RA) to form the seed money for the CPF Life scheme.

If you set aside this sum in your RA then, you can start to receive monthly payouts of about $1,620 once you turn 65.

But if you feel that this sum is not enough, you can voluntarily increase it to $2,370 a month by opting to set aside the enhanced retirement sum ($298,200 in 2023) when you hit 55. This can be done by topping up your RA with a further $99,400, either by transferring cash from your bank account or from funds in your CPF Special and Ordinary Accounts.

The better way is to plan for a stable and continuous income that can last a lifetime so that you can continue to pay for your expenses, which certainly don’t stop once you finish working.

If you need $3,000 a month, for example, you must have at least $720,000 to last you from age 65 to 85.

If you have set aside the enhanced retirement sum (ERS) for CPF Life when you hit 55 in 2023, you can receive payouts of $2,370 a month from 65, which would have reached a total of $568,800 when you hit 85.

If you have such payouts, you will need to withdraw only about $600 more from your savings every month, or about $150,000 during those two decades.

Given a choice, you would likely want to narrow the gap between your expected expenses and lifelong income. This is probably why some participants of Forward Singapore wanted the option of being able to save more for their CPF Life in order to get bigger payouts.

The Forward Singapore report that covers the initiatives to “ensure seniors retire with peace of mind” noted that there are groups of people who would like to put even more into their RA so that they can benefit from higher CPF Life payouts.

“We will therefore review and raise the enhanced retirement sum to enable more Singaporeans to receive higher payouts in retirement,” the report added.

Pending the announcement on how much more you can save, you should take note of these three tips on CPF Life that will help you plan.

While it is not compulsory to keep up to date with the required annual sums for those who are already 55 or older, you can make annual top-ups with every increase so that your payout gets a small boost.

For instance, setting aside $298,200 for 2023’s ERS will get you a monthly payout of $2,370 from age 65. When the ERS becomes $308,700 in 2024, you can choose to top up the difference, or $10,500, to get a monthly payout of $2,450.

That additional $80 a month may not seem a lot at first glance but if you keep topping up annually, the payout would be $2,690, over $300 more, if you match the ERS in 2027, which is $342,300.

The difference is quite significant for seniors who have not kept up to date with the increases over the past decade.

For instance, those who turned 55 in 2016 could set aside only $241,500 for the ERS then to get up to $1,900 in monthly payouts. For a start, these seniors could make over $50,000 in top-ups to hit the limit set for this year.

Doing so may not automatically increase their payout to $2,370 when they reach 65 because they have missed out on the extra earnings in the last seven years. But it is worth booking an appointment with the CPF Board to learn how they can catch up and get more lifelong income.

A couple who both turn 55 in 2023 and set aside the ERS of $298,200 each, or $596,400 in total, will get a combined payout of about $4,700 when they hit 65.

So setting aside about $600,000 will enable you and your spouse to get lifelong income of close to $5,000 a month when you turn 65. In 20 years’ times, both of you would have received more than $1.1 million in payouts.

MORE ON THIS TOPIC

When couples fight over their CPF money during divorce

How you can shield your CPF and bank accounts from scammers

Many people think that having an extra property to generate rental income in their old age is the way to go. In doing so, they deplete their CPF savings and miss out on the opportunity to earn such good income as a couple.

Consider this instead: Make sure both of you can hit the ERS tier for CPF Life to get a good lifelong income. If you still have ample cash, you can consider your two-property dream.

CPF Life is a far cheaper and better annuity because its return is much higher dollar for dollar, more stable and will pay you for life. This is possible only because the non-profit scheme is backed by the Government.

So it makes absolutely no sense, especially for those in their 50s, to ask financial institutions about products for retirement planning if you have not even maxed out your CPF Life contributions. This is akin to paying for a more expensive product that will pay less because you don’t realise that there is a far cheaper and better scheme that pays more.

The good news for seniors below 80 who have missed out on this deal is that it is never too late to get back into the game as you can make cash top-ups directly to your RA.

Before you do so, invest the time to visit the CPF Board and learn for yourself why CPF Life is so desirable. After all, many savvy Singaporeans are actually telling the Government that they want to put more money in there.

On this count, this is similar to a Ponzi scheme: asking Sinkies for more money so that those who want to withdraw will be paid.

How to earn good lifelong income from your CPF

CPF Life is a far cheaper and better annuity than private annuities because its return is much higher dollar for dollar, more stable and will pay you for life. ZAOBAO FILE PHOTO

Tan Ooi Boon

Invest Editor

NOV 12, 2023

Retirement planning for many people here just got a boost, thanks to some participants of the Forward Singapore dialogues who shared their views on the importance of having continuous and stable income in old age.

Their input has prompted the Government to look at tweaking the voluntary component of the CPF Life annuity scheme to allow members to increase their savings in readiness for their golden years.

As it stands now, when members reach 55, the full retirement sum ($198,800 this year) will be moved from their CPF accounts to their Retirement Account (RA) to form the seed money for the CPF Life scheme.

If you set aside this sum in your RA then, you can start to receive monthly payouts of about $1,620 once you turn 65.

But if you feel that this sum is not enough, you can voluntarily increase it to $2,370 a month by opting to set aside the enhanced retirement sum ($298,200 in 2023) when you hit 55. This can be done by topping up your RA with a further $99,400, either by transferring cash from your bank account or from funds in your CPF Special and Ordinary Accounts.

Lifelong income is critical

One of life’s hard truths is that our savings alone may not be enough to fund a comfortable retirement unless we have an unusually large pot of cash or are astute investors who know how to keep growing our money.The better way is to plan for a stable and continuous income that can last a lifetime so that you can continue to pay for your expenses, which certainly don’t stop once you finish working.

If you need $3,000 a month, for example, you must have at least $720,000 to last you from age 65 to 85.

If you have set aside the enhanced retirement sum (ERS) for CPF Life when you hit 55 in 2023, you can receive payouts of $2,370 a month from 65, which would have reached a total of $568,800 when you hit 85.

If you have such payouts, you will need to withdraw only about $600 more from your savings every month, or about $150,000 during those two decades.

Given a choice, you would likely want to narrow the gap between your expected expenses and lifelong income. This is probably why some participants of Forward Singapore wanted the option of being able to save more for their CPF Life in order to get bigger payouts.

The Forward Singapore report that covers the initiatives to “ensure seniors retire with peace of mind” noted that there are groups of people who would like to put even more into their RA so that they can benefit from higher CPF Life payouts.

“We will therefore review and raise the enhanced retirement sum to enable more Singaporeans to receive higher payouts in retirement,” the report added.

Pending the announcement on how much more you can save, you should take note of these three tips on CPF Life that will help you plan.

Increasing payouts with annual top-ups

Those who turn 55 in 2023 are setting aside retirement sums that are about 3.5 per cent higher than those paid by the cohort in 2022. The sum goes up annually so that members can receive gradual increases in payouts as a way to counter inflation.While it is not compulsory to keep up to date with the required annual sums for those who are already 55 or older, you can make annual top-ups with every increase so that your payout gets a small boost.

For instance, setting aside $298,200 for 2023’s ERS will get you a monthly payout of $2,370 from age 65. When the ERS becomes $308,700 in 2024, you can choose to top up the difference, or $10,500, to get a monthly payout of $2,450.

That additional $80 a month may not seem a lot at first glance but if you keep topping up annually, the payout would be $2,690, over $300 more, if you match the ERS in 2027, which is $342,300.

The difference is quite significant for seniors who have not kept up to date with the increases over the past decade.

For instance, those who turned 55 in 2016 could set aside only $241,500 for the ERS then to get up to $1,900 in monthly payouts. For a start, these seniors could make over $50,000 in top-ups to hit the limit set for this year.

Doing so may not automatically increase their payout to $2,370 when they reach 65 because they have missed out on the extra earnings in the last seven years. But it is worth booking an appointment with the CPF Board to learn how they can catch up and get more lifelong income.

It pays to plan as a couple

Couples get more bang for their buck than singles because they can enjoy two sets of CPF Life payouts, which will be quite decent if both are in the ERS tier.A couple who both turn 55 in 2023 and set aside the ERS of $298,200 each, or $596,400 in total, will get a combined payout of about $4,700 when they hit 65.

So setting aside about $600,000 will enable you and your spouse to get lifelong income of close to $5,000 a month when you turn 65. In 20 years’ times, both of you would have received more than $1.1 million in payouts.

When couples fight over their CPF money during divorce

How you can shield your CPF and bank accounts from scammers

Many people think that having an extra property to generate rental income in their old age is the way to go. In doing so, they deplete their CPF savings and miss out on the opportunity to earn such good income as a couple.

Consider this instead: Make sure both of you can hit the ERS tier for CPF Life to get a good lifelong income. If you still have ample cash, you can consider your two-property dream.

CPF Life before private annuity

Some people prefer buying private annuities instead of putting more money in CPF Life because they are not aware that it is the best deal in town.CPF Life is a far cheaper and better annuity because its return is much higher dollar for dollar, more stable and will pay you for life. This is possible only because the non-profit scheme is backed by the Government.

So it makes absolutely no sense, especially for those in their 50s, to ask financial institutions about products for retirement planning if you have not even maxed out your CPF Life contributions. This is akin to paying for a more expensive product that will pay less because you don’t realise that there is a far cheaper and better scheme that pays more.

The good news for seniors below 80 who have missed out on this deal is that it is never too late to get back into the game as you can make cash top-ups directly to your RA.

Before you do so, invest the time to visit the CPF Board and learn for yourself why CPF Life is so desirable. After all, many savvy Singaporeans are actually telling the Government that they want to put more money in there.

Asking Sinkies to put more money into CPF instead of using their CPF savings to buy property.

What is the motive?

The national annuity scheme can yield far better dollar-for-dollar returns than a rental property. PHOTO: ST FILE

Tan Ooi Boon

Invest Editor

JUN 12, 2023

It is impossible to buy an apartment for $600,000 that can guarantee you a monthly income of about $5,000 in today’s red-hot property market, but the Central Provident Fund’s (CPF) annuity scheme can give a couple such returns.

If a couple want to enjoy such a bumper monthly income for life with that same amount of savings, they can start planning with the aim of joining CPF Life at the highest tier when they reach the age of 55.

Many people do not realise that the national annuity scheme, which provides a good lifelong income for retirees, can yield far better dollar-for-dollar returns than a rental property.

Just like Singapore Savings Bonds or Treasury Bills, there is nothing to dislike about CPF Life because it works just like any annuity scheme in the market, except that it is much cheaper to take up and provides a stable monthly income for life because it is backed by the Government.

Yet, many people choose not to make better use of it, preferring instead to put their money into a second property, for instance, thinking it can provide a higher retirement income.

Those who do so often risk having their plans go awry when unfavourable economic conditions affect their plans, such as when the rental income is eroded due to higher mortgage rates.

Here are three reasons why CPF Life can provide better benefits to a retired couple, than having another property for rental income.

You don’t need such high outlays for CPF Life because you can join the scheme based on what you can afford.

For instance, those hitting 55 who join with the Full Retirement Sum (FRS) of $198,800 in 2023 will stand to get about $1,600 a month from the age of 65, while those putting up the Enhanced Retirement Sum (ERS) of $298,200 will get about $2,400.

So a couple who put up about $400,000 can stand to get a combined lifelong retirement income of $3,200 a month, while those signing up with about $600,000 can get around $4,800 in total.

If they live up to 90, they would have received $960,000 (FRS) and $1.44 million (ERS) in total payouts.

If you have the misfortune of ending up with tenants from hell, you may even have to spend hefty legal fees to resolve such nightmares.

Retired couples who have decent CPF Life payments don’t have such risks because there are no fees to pay and the payouts are tax-free. Indeed, those who don’t have high monthly expenses can even save a portion of these payouts for their annual holidays, without touching their savings.

CPF Life payouts are stable and not as volatile as other private financial products. Indeed, you can even choose to increase your monthly payouts by making annual top-ups of up to $10,000 to the scheme.

Of course, it is all well and good if you can invest in extra properties for your retirement, but you should not miss out on the best deal in town that can provide a decent lifelong income for only a fraction of the price of a property.

The reality is that many property owners do encounter cashflow problems in their old age, so CPF payouts can help meet some of their bills. This has prompted some retirees to sell their properties so they can use part of the proceeds to join CPF Life, as long as they are under 80.

While their payouts won’t be as good as those who joined at 55, it is still better late than never to enjoy fuss-free cash payouts for life.

Finally, couples in their prime looking to plan for a good retirement should first do the sums for CPF Life before embarking on buying a second property. Don’t miss out the chance to secure a sound asset that will continuously give you payouts through your golden years.

What is the motive?

Why CPF Life can be better than an investment property

The national annuity scheme can yield far better dollar-for-dollar returns than a rental property. PHOTO: ST FILE

Tan Ooi Boon

Invest Editor

JUN 12, 2023

It is impossible to buy an apartment for $600,000 that can guarantee you a monthly income of about $5,000 in today’s red-hot property market, but the Central Provident Fund’s (CPF) annuity scheme can give a couple such returns.

If a couple want to enjoy such a bumper monthly income for life with that same amount of savings, they can start planning with the aim of joining CPF Life at the highest tier when they reach the age of 55.

Many people do not realise that the national annuity scheme, which provides a good lifelong income for retirees, can yield far better dollar-for-dollar returns than a rental property.

Just like Singapore Savings Bonds or Treasury Bills, there is nothing to dislike about CPF Life because it works just like any annuity scheme in the market, except that it is much cheaper to take up and provides a stable monthly income for life because it is backed by the Government.

Yet, many people choose not to make better use of it, preferring instead to put their money into a second property, for instance, thinking it can provide a higher retirement income.

Those who do so often risk having their plans go awry when unfavourable economic conditions affect their plans, such as when the rental income is eroded due to higher mortgage rates.

Here are three reasons why CPF Life can provide better benefits to a retired couple, than having another property for rental income.

Affordability

Not everyone can be a landlord because it is expensive to invest in a second property. Even if you can buy one, you must be prepared to pay over $1 million for a better unit if you want to earn a higher rent.You don’t need such high outlays for CPF Life because you can join the scheme based on what you can afford.

For instance, those hitting 55 who join with the Full Retirement Sum (FRS) of $198,800 in 2023 will stand to get about $1,600 a month from the age of 65, while those putting up the Enhanced Retirement Sum (ERS) of $298,200 will get about $2,400.

So a couple who put up about $400,000 can stand to get a combined lifelong retirement income of $3,200 a month, while those signing up with about $600,000 can get around $4,800 in total.

If they live up to 90, they would have received $960,000 (FRS) and $1.44 million (ERS) in total payouts.

Tax- and hassle-free

Landlords don’t just pocket the rent; there are various costs to meet before they can earn real income. These include income and property taxes, mortgage payments, estate maintenance charges, costs for repairs, and replacement of household items, plus fees for finding tenants.If you have the misfortune of ending up with tenants from hell, you may even have to spend hefty legal fees to resolve such nightmares.

Retired couples who have decent CPF Life payments don’t have such risks because there are no fees to pay and the payouts are tax-free. Indeed, those who don’t have high monthly expenses can even save a portion of these payouts for their annual holidays, without touching their savings.

Stable income

Rental income is dependent on the state of your property as well as market conditions. If times are bad, there is a risk that you may not have a rental income. While you can sell your property, the proceeds will not last forever unless you know how to invest prudently.CPF Life payouts are stable and not as volatile as other private financial products. Indeed, you can even choose to increase your monthly payouts by making annual top-ups of up to $10,000 to the scheme.

Of course, it is all well and good if you can invest in extra properties for your retirement, but you should not miss out on the best deal in town that can provide a decent lifelong income for only a fraction of the price of a property.

The reality is that many property owners do encounter cashflow problems in their old age, so CPF payouts can help meet some of their bills. This has prompted some retirees to sell their properties so they can use part of the proceeds to join CPF Life, as long as they are under 80.

While their payouts won’t be as good as those who joined at 55, it is still better late than never to enjoy fuss-free cash payouts for life.

Finally, couples in their prime looking to plan for a good retirement should first do the sums for CPF Life before embarking on buying a second property. Don’t miss out the chance to secure a sound asset that will continuously give you payouts through your golden years.

Putting money in CPF Life is better than buying annuity plans from private insurers wor.....

Annuities have become popular in recent years as people focus on the relatively lower risk of the products as well as the regular payouts they can offer. ST PHOTO: LIM YAOHUI

Lee Su Shyan

Associate Editor & Senior Columnist

OCT 16, 2023

Q: I am considering buying an annuity as one way to supplement the payouts from CPF Life (Lifelong Income for the Elderly). What are the pros and cons?

Many people approaching retirement are hoping to maintain a standard of living close to what they have when they are working. While CPF Life – the national longevity insurance annuity scheme – provides monthly payouts for life, it may not be sufficient should people be aiming for a more luxurious lifestyle.

While investments can bring in higher returns than an annuity, some feel they are not well versed enough to put their money into investments or are put off by the risks.

Accordingly, annuities have become popular in recent years as people focus on the relatively lower risk of the products as well as the regular payouts they can offer.

Phillip Securities’ financial services associate director Leslie Ng estimates that a 45-year-old male can achieve a $1,000 monthly lifetime payout (comprising guaranteed and non-guaranteed components) from age 65 if he saves $1,000 a month for 15 years, or $1,400 per month for 10 years. He can also set aside $128,000 in a single premium at the age of 45.

This will give him additional income on top of his CPF Life payouts for added assurance in his retirement years.

At the age of 55, your Central Provident Fund savings will be transferred, up to the Full Retirement Sum (FRS), to create your Retirement Account (RA), which will provide the monthly payouts in your retirement.

For the 2023 cohort of people who turn 55 during the year, the FRS is $198,800. With this amount in the RA, this translates to an estimated monthly payout of between $1,510 and $1,620, starting from the age of 65, based on the CPF Life Standard Plan.

An individual can keep more in the RA, but the amount is limited to the prevailing Enhanced Retirement Sum (ERS) of the year.

The prevailing ERS in 2023 is $298,200. This translates to monthly payouts of between $2,210 and $2,370 for life, based on the CPF Life Standard Plan.

The earliest that you can commence your CPF Life payouts is at age 65. You can also opt to defer them till age 70.

A life annuity provides monthly or yearly payouts for as long as you live and insures you against the risk of outliving your savings. It involves paying an insurer a one-time single premium or a series of payments over an agreed period. The premium is invested to provide you with regular income in the future.

As most retirees worry about outliving their financial resources, the annuity’s regular payouts – especially if they are guaranteed and for life – offer them peace of mind, Ms Tan said.

There is also the added plus that should the insured die prematurely, the balance cash value, if any, will be distributed to his beneficiaries, she added.

As CPF Life payouts start at 65, “if you desire an earlier income flow, you may consider an immediate annuity that is designed to pay an income soon after it is bought”, she said.

The additional income stream from the annuity comes in handy to supplement the CPF Life payouts. “Most retirees find themselves spending more in the first 10 to 20 years of their retirement as they would be more physically mobile and desire to travel or pursue passions like setting up a small business,” she added.

MORE ON THIS TOPIC

Why CPF Life can be better than an investment property

More in S'pore choosing to spend on health than on luxury items: Poll

Phillip Securities’ Mr Ng said people can choose whether to receive the annuity payouts over 10 or 20 years, or over their entire lifetime. “As people become more aware of their increasing life expectancy, we are seeing them plan for lifetime payouts.”

He said he has seen more inquiries from clients aged 40 and above. “This stems from their realisation that many ongoing costs are inescapable even in our retirement – one of which is our Integrated Shield premiums, which increase with age and medical inflation. We therefore need to create an income stream for such necessities.”

That’s because as people age, it is possible that the additional private medical insurance premium payable on the Integrated Shield Plan will exceed the MediSave withdrawable limits, requiring a cash top-up of the difference.

Mr Ng added: “Nowadays, I rarely see clients with only one retirement plan. Instead, they combine multiple plans so that they can have a higher monthly payout during their active retirement years from age 65 to 75, and a lower payout from age 75 onwards.”

Mr Christopher Tan, chief executive of wealth advisory firm Providend, said: “The advantage of such products is that you can buy at any time you want and decide when you want to have the payout. There are no restrictions like those for CPF Life, where the earliest you can have the payout is age 65.”

He added that people can surrender their annuity/retirement income products halfway and encash the surrender value if they are prepared to suffer some losses. There is no such option with CPF Life.

Another feature that customers have been drawn to is the flexibility to change the life insured and assign the policy to the next generation.

Mr Raymond Ong, CEO of Etiqa Insurance Singapore, said this means “the policy can be passed down to the next generation while the regular income is being paid”.

These retirement insurance products are now getting popular for estate planning. With the option for beneficiaries to receive payments even after the policyholder’s death, this can provide lifetime income to the surviving spouse and family.

Mr Ong added that the retirement policies often come with a short payment term, such as between three and five years, to make the premium more affordable, instead of a large single payment.

They also have features such as flexible payout options, where one can deposit the money with the insurer at a non-guaranteed interest rate, with the flexibility of withdrawing it at any time the money is needed.

Some of these policies can offer inflation protection, which ensures that the income keeps pace with the rising cost of living.

Note that CPF Life also offers a similar option to protect your retirement income from rising prices with its Escalating Plan, under which payouts will increase by 2 per cent each year. The payouts start lower, but eventually become higher than the Standard Plan and Basic Plan payouts.

These products generally will offer a regular monthly stream of income as well as a lump-sum payout at retirement. You can choose the payout period as well as the sum you want per month.

You can even make changes to the income payout period, but do check at what point this needs to be done.

Another feature will allow you to put your premium payment on hold while your policy stays in force – for example, during a period of retrenchment.

These plans may also offer the waiver of premiums where there is total and permanent disability.

Another important point to note is that for the payouts, there is usually a guaranteed portion and a non-guaranteed component, which can fluctuate.

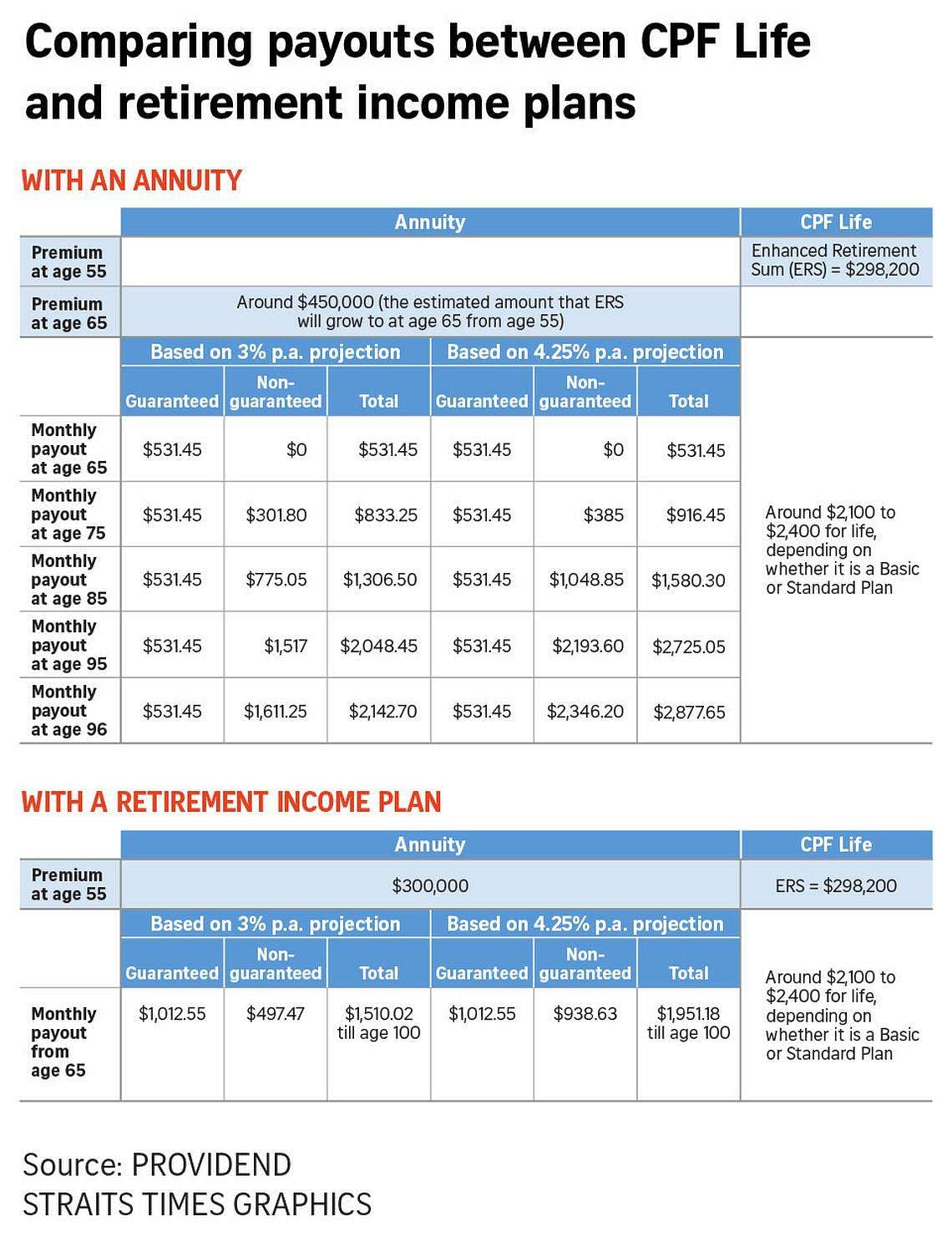

Providend’s Mr Tan said the reason CPF Life can offer higher returns is that the Singapore Government guarantees the return – based on a formula – as well as the capital from any losses. In addition, there is no distribution cost and so expenses are much lower, which in turn translates to higher returns, he added.

He said CPF Life is Singapore’s best annuity plan, but there is a limit to how much one can “buy” of CPF Life.

He used an illustration to compare CPF Life, based on the ERS amount of $298,200, with a near-equivalent amount placed in an annuity and retirement plan with an insurance company in Singapore (see tables).

This comparison shows that the guaranteed portion compared with CPF Life is lower. Even if the insurer can achieve the projected returns for the non-guaranteed portion, the two amounts added together is still lower than the CPF Life payout, noted Mr Tan.

CPF says that if you have a pension or private annuity plan that provides the same or higher monthly payouts for life, you can apply to be exempted from setting aside the retirement sum, and withdraw all your CPF retirement savings.

Exemption from CPF Life is allowed from age 55, as long as the member is receiving guaranteed monthly annuity payouts at the point of application to be exempted.

Take, for instance, someone who turns 55 in 2023, when the FRS is $198,800. In order to be exempted from CPF Life and withdraw this sum, a male CPF member would need to have an annuity that provides a guaranteed monthly annuity payout of at least $1,628, or at least $1,517 in the case of a female CPF member.

The member has to be both the policyholder and the sole insured person of the annuity policy.

Take note that if some time down the road, you surrender or terminate your annuity, that surrender value must be refunded to your RA, up to the Full Retirement Sum applicable to you, with accrued interest.

Mr Gregory Chia, group director of retirement income at CPF Board, said: “While there is this option to get exempted from CPF Life if you have a private annuity, we have not seen members taking up this option in recent years.

“It indicates that members themselves find CPF Life to be superior to other annuities in the market. If they do buy annuities, it is in addition to CPF Life, rather than to replace it.”

DBS’ Ms Tan said there are also investment products such as funds that can offer similar regular income payouts.

Especially for those who are in paid employment, probably the most straightforward way of retirement planning is to focus on achieving the requisite ERS.

Flexible features of annuities draw investors as a supplement to CPF Life

This regular column addresses readers’ investing issues.

Annuities have become popular in recent years as people focus on the relatively lower risk of the products as well as the regular payouts they can offer. ST PHOTO: LIM YAOHUI

Lee Su Shyan

Associate Editor & Senior Columnist

OCT 16, 2023

Q: I am considering buying an annuity as one way to supplement the payouts from CPF Life (Lifelong Income for the Elderly). What are the pros and cons?

Many people approaching retirement are hoping to maintain a standard of living close to what they have when they are working. While CPF Life – the national longevity insurance annuity scheme – provides monthly payouts for life, it may not be sufficient should people be aiming for a more luxurious lifestyle.

While investments can bring in higher returns than an annuity, some feel they are not well versed enough to put their money into investments or are put off by the risks.

Accordingly, annuities have become popular in recent years as people focus on the relatively lower risk of the products as well as the regular payouts they can offer.

Phillip Securities’ financial services associate director Leslie Ng estimates that a 45-year-old male can achieve a $1,000 monthly lifetime payout (comprising guaranteed and non-guaranteed components) from age 65 if he saves $1,000 a month for 15 years, or $1,400 per month for 10 years. He can also set aside $128,000 in a single premium at the age of 45.

This will give him additional income on top of his CPF Life payouts for added assurance in his retirement years.

CPF Life

But first things first. Financial advisers generally say that CPF Life is the foundation for retirement planning.At the age of 55, your Central Provident Fund savings will be transferred, up to the Full Retirement Sum (FRS), to create your Retirement Account (RA), which will provide the monthly payouts in your retirement.

For the 2023 cohort of people who turn 55 during the year, the FRS is $198,800. With this amount in the RA, this translates to an estimated monthly payout of between $1,510 and $1,620, starting from the age of 65, based on the CPF Life Standard Plan.

An individual can keep more in the RA, but the amount is limited to the prevailing Enhanced Retirement Sum (ERS) of the year.

The prevailing ERS in 2023 is $298,200. This translates to monthly payouts of between $2,210 and $2,370 for life, based on the CPF Life Standard Plan.

The earliest that you can commence your CPF Life payouts is at age 65. You can also opt to defer them till age 70.

Annuities in a nutshell

Annuities are often described as retirement income insurance nowadays. They fall into two types, said DBS Bank’s head of financial planning literacy Lorna Tan. Traditional or life annuities provide cash flow for the rest of one’s lifetime. Term annuities provide cash flow for a specific period.A life annuity provides monthly or yearly payouts for as long as you live and insures you against the risk of outliving your savings. It involves paying an insurer a one-time single premium or a series of payments over an agreed period. The premium is invested to provide you with regular income in the future.

As most retirees worry about outliving their financial resources, the annuity’s regular payouts – especially if they are guaranteed and for life – offer them peace of mind, Ms Tan said.

There is also the added plus that should the insured die prematurely, the balance cash value, if any, will be distributed to his beneficiaries, she added.

As CPF Life payouts start at 65, “if you desire an earlier income flow, you may consider an immediate annuity that is designed to pay an income soon after it is bought”, she said.

The additional income stream from the annuity comes in handy to supplement the CPF Life payouts. “Most retirees find themselves spending more in the first 10 to 20 years of their retirement as they would be more physically mobile and desire to travel or pursue passions like setting up a small business,” she added.

Why CPF Life can be better than an investment property

More in S'pore choosing to spend on health than on luxury items: Poll

Phillip Securities’ Mr Ng said people can choose whether to receive the annuity payouts over 10 or 20 years, or over their entire lifetime. “As people become more aware of their increasing life expectancy, we are seeing them plan for lifetime payouts.”

He said he has seen more inquiries from clients aged 40 and above. “This stems from their realisation that many ongoing costs are inescapable even in our retirement – one of which is our Integrated Shield premiums, which increase with age and medical inflation. We therefore need to create an income stream for such necessities.”

That’s because as people age, it is possible that the additional private medical insurance premium payable on the Integrated Shield Plan will exceed the MediSave withdrawable limits, requiring a cash top-up of the difference.

Mr Ng added: “Nowadays, I rarely see clients with only one retirement plan. Instead, they combine multiple plans so that they can have a higher monthly payout during their active retirement years from age 65 to 75, and a lower payout from age 75 onwards.”

Mr Christopher Tan, chief executive of wealth advisory firm Providend, said: “The advantage of such products is that you can buy at any time you want and decide when you want to have the payout. There are no restrictions like those for CPF Life, where the earliest you can have the payout is age 65.”

He added that people can surrender their annuity/retirement income products halfway and encash the surrender value if they are prepared to suffer some losses. There is no such option with CPF Life.

Another feature that customers have been drawn to is the flexibility to change the life insured and assign the policy to the next generation.

Mr Raymond Ong, CEO of Etiqa Insurance Singapore, said this means “the policy can be passed down to the next generation while the regular income is being paid”.

These retirement insurance products are now getting popular for estate planning. With the option for beneficiaries to receive payments even after the policyholder’s death, this can provide lifetime income to the surviving spouse and family.

Mr Ong added that the retirement policies often come with a short payment term, such as between three and five years, to make the premium more affordable, instead of a large single payment.

They also have features such as flexible payout options, where one can deposit the money with the insurer at a non-guaranteed interest rate, with the flexibility of withdrawing it at any time the money is needed.

Some of these policies can offer inflation protection, which ensures that the income keeps pace with the rising cost of living.

Note that CPF Life also offers a similar option to protect your retirement income from rising prices with its Escalating Plan, under which payouts will increase by 2 per cent each year. The payouts start lower, but eventually become higher than the Standard Plan and Basic Plan payouts.

Some features of annuities

There are several players in the market that offer retirement income insurance. Apart from DBS, Etiqa Insurance Singapore, Great Eastern, Income, Manulife and Prudential are among those that have such products in the market.These products generally will offer a regular monthly stream of income as well as a lump-sum payout at retirement. You can choose the payout period as well as the sum you want per month.

You can even make changes to the income payout period, but do check at what point this needs to be done.

Another feature will allow you to put your premium payment on hold while your policy stays in force – for example, during a period of retrenchment.

These plans may also offer the waiver of premiums where there is total and permanent disability.

What to watch out for

These retirement income plans may offer more flexibility than CPF Life, but are likely to fall short when it comes to the payouts. DBS’ Ms Tan cautioned that private insurers will find it difficult to match CPF Life’s guaranteed and risk-free interest rate, which can go up to 6 per cent a year.Another important point to note is that for the payouts, there is usually a guaranteed portion and a non-guaranteed component, which can fluctuate.

Providend’s Mr Tan said the reason CPF Life can offer higher returns is that the Singapore Government guarantees the return – based on a formula – as well as the capital from any losses. In addition, there is no distribution cost and so expenses are much lower, which in turn translates to higher returns, he added.

He said CPF Life is Singapore’s best annuity plan, but there is a limit to how much one can “buy” of CPF Life.

He used an illustration to compare CPF Life, based on the ERS amount of $298,200, with a near-equivalent amount placed in an annuity and retirement plan with an insurance company in Singapore (see tables).

This comparison shows that the guaranteed portion compared with CPF Life is lower. Even if the insurer can achieve the projected returns for the non-guaranteed portion, the two amounts added together is still lower than the CPF Life payout, noted Mr Tan.

Being exempted from CPF Life

The savings in your RA are meant to provide you with monthly payouts during retirement.CPF says that if you have a pension or private annuity plan that provides the same or higher monthly payouts for life, you can apply to be exempted from setting aside the retirement sum, and withdraw all your CPF retirement savings.

Exemption from CPF Life is allowed from age 55, as long as the member is receiving guaranteed monthly annuity payouts at the point of application to be exempted.

Take, for instance, someone who turns 55 in 2023, when the FRS is $198,800. In order to be exempted from CPF Life and withdraw this sum, a male CPF member would need to have an annuity that provides a guaranteed monthly annuity payout of at least $1,628, or at least $1,517 in the case of a female CPF member.

The member has to be both the policyholder and the sole insured person of the annuity policy.

Take note that if some time down the road, you surrender or terminate your annuity, that surrender value must be refunded to your RA, up to the Full Retirement Sum applicable to you, with accrued interest.

Mr Gregory Chia, group director of retirement income at CPF Board, said: “While there is this option to get exempted from CPF Life if you have a private annuity, we have not seen members taking up this option in recent years.

“It indicates that members themselves find CPF Life to be superior to other annuities in the market. If they do buy annuities, it is in addition to CPF Life, rather than to replace it.”

Bottom line

Annuities will not stack up based on the numbers, but may be an option for those who are looking to supplement their CPF Life.DBS’ Ms Tan said there are also investment products such as funds that can offer similar regular income payouts.

Especially for those who are in paid employment, probably the most straightforward way of retirement planning is to focus on achieving the requisite ERS.

Trying to CONvince Sinkies to voluntarily put more money into the Ponzi scheme. Oops! CPF, not Ponzi.

Are you heading for a comfortable retirement? In this edition of Money Matters, we learn how Singaporeans can make the most of their Central Provident Fund (CPF) savings to build up their retirement nest egg that can continue growing for years.

Chor Khieng Yuit

Senior Correspondent

MAY 6, 2023

SINGAPORE – Hitting 55 is a significant milestone for many Singaporeans – it’s that much closer to retirement and also the age when we can withdraw some of our Central Provident Fund (CPF) savings.

But don’t open the bubbly too quickly – about 33 per cent of active CPF members who turned 55 in 2022 have not set aside the Full Retirement Sum in their CPF savings or in CPF savings and property, noted the Ministry of Manpower (MOM).

About 45 per cent of those who failed to set aside the Full Retirement Sum were male.

MOM estimated that about 24 per cent of active CPF members will fail to set aside the Full Retirement Sum over the next five years, down from about 33 per cent in 2022.

So how can you boost your CPF savings for retirement?

The amount transferred will be the Full Retirement Sum for the year, which is $198,800 in 2023.

Ms Lorna Tan, head of financial planning literacy at DBS Bank, says that by starting early, “it is possible to grow CPF balances to at least the Full Retirement Sum at age 55”, even if you start small because you have time on your side.

You can also top up your SA with cash to the Full Retirement Sum and get a tax relief of up to $8,000 per calendar year.

Ms Tan says CPF members should do their top-ups at the beginning of the year, noting: “As CPF interest is calculated monthly, if a CPF member makes a top-up in January instead of December each year, he will earn 20 per cent more in interest over 10 years.”

CPF members who have turned 55 can also set aside more for retirement by transferring their OA and SA savings to their RA up to the Enhanced Retirement Sum, which is $298,200 in 2023.

You can also top up with cash to the Enhanced Retirement Sum, but you will not qualify for the $8,000 tax relief.

Tax relief applies only for cash top-ups to the Full Retirement Sum. Top-ups above this up to the Enhanced Retirement Sum of $298,200 this year will not qualify.

If you set aside only the Full Retirement Sum instead of topping up to the Enhanced Retirement Sum, you can just leave your remaining CPF money in your OA and SA, where it will continue to earn interest.

After you turn 55, the yearly increase in the Full Retirement Sum does not affect you any more. The Full Retirement Sum you need to set aside depends on when you turn 55 and is fixed for the rest of your life. However, you can continue to set aside up to the prevailing Enhanced Retirement Sum.

DBS’ Ms Tan says these top-ups go into Ordinary, Special and MediSave Accounts, up to $37,740, known as the CPF Annual Limit.

The maximum amount of voluntary contributions to the three CPF accounts is the difference between this annual limit and the amount of mandatory CPF contributions received for the year, Ms Tan adds.

Voluntary contributions do not enjoy tax relief, unlike cash top-ups under the Retirement Sum Topping-up Scheme.

Ms Tan says making voluntary contributions may be a great idea if you have excess cash that you do not need in the near term, but it may not work if you are in a tight financial situation and need money for more pressing things.

She adds that the CPF Voluntary Contribution Scheme is useful for senior members who have lower mandatory contributions as they grow older.

These members can set aside half of the Full Retirement Sum, which is the Basic Retirement Sum if they own a property. This Basic Retirement Sum is $99,400 in 2023.

Ms Tan says these members will have to restore their RA back to the Full Retirement Sum with the proceeds when they eventually sell their property.

She adds that there will be a second transfer of CPF savings to the RA, at the payout start age, which can be any time from age 65 to 70.

This applies to those born in 1958 or later, and who have not met their Full Retirement Sum by 55.

CPF members who have to stop working have options as well.

Ms Tay Mui Huang, senior adviser at Financial Alliance, says their spouses can transfer some of their CPF savings to their CPF accounts. Their spouses can also do a cash top-up for them up to the current Full Retirement Sum. These top-ups can bring tax relief of up to $8,000 a year.

She adds that SA shielding should be done a few weeks before a member turns 55.

“Leave behind $40,000, which is the minimum amount that a member needs to keep in his SA. Invest the rest temporarily in a short-term and relatively safe investment product under the CPF Investment Scheme,” Ms Tan notes.

When the member turns 55, $40,000 from his SA and savings from his OA – up to the Full Retirement Sum – will be transferred to his RA.

“The CPF member can then liquidate his temporary investment, and the amount invested plus gains (if any) will return to his SA,” Ms Tan says.

This allows the CPF member to retain most of his SA savings, which will continue to earn interest at 4 per cent a year.

You can withdraw this interest earned regularly, effectively getting a “passive income stream to fund retirement needs”, Ms Tan notes.

The rest of the SA savings can stay in the CPF to compound and earn interest every year, she adds, likening this to a “fixed deposit with interest of 4 per cent per annum”.

But Ms Tan urges being careful when picking an investment product to park your SA savings temporarily. “If the fund value drops during the investment period, the CPF member may have to stomach losses on his SA savings, or he may consider liquidating it later.”

MORE ON THIS TOPIC

More people voluntarily contributing to retirement scheme amid uncertainties

4 myths that stop some from enjoying CPF’s benefits

You can withdraw this money at any time after 55, whether in full or partially.

The CPF Board notes: “If the member subsequently decides to put back the money in his CPF, he can do so by topping back up to the prevailing Enhanced Retirement Sum. This top-up will, however, not qualify for tax reliefs.”

Ms Tan adds that CPF members born in 1958 or later “can withdraw an additional amount of up to 20 per cent of their retirement savings at 65”.

However, you will not be able to withdraw cash top-ups or CPF transfers you have made to your retirement savings, she says, adding that you also cannot withdraw government grants to your CPF such as the CPF Life Bonus.

“CPF members will also need to be mindful that they are forgoing risk-free interest that they will otherwise earn if they leave the money in their CPF accounts,” Ms Tan adds.

How to maximise CPF savings to grow your nest egg for retirement

Are you heading for a comfortable retirement? In this edition of Money Matters, we learn how Singaporeans can make the most of their Central Provident Fund (CPF) savings to build up their retirement nest egg that can continue growing for years.

Chor Khieng Yuit

Senior Correspondent

MAY 6, 2023

SINGAPORE – Hitting 55 is a significant milestone for many Singaporeans – it’s that much closer to retirement and also the age when we can withdraw some of our Central Provident Fund (CPF) savings.

But don’t open the bubbly too quickly – about 33 per cent of active CPF members who turned 55 in 2022 have not set aside the Full Retirement Sum in their CPF savings or in CPF savings and property, noted the Ministry of Manpower (MOM).

About 45 per cent of those who failed to set aside the Full Retirement Sum were male.

MOM estimated that about 24 per cent of active CPF members will fail to set aside the Full Retirement Sum over the next five years, down from about 33 per cent in 2022.

So how can you boost your CPF savings for retirement?

1. Build up these savings early to benefit from compounding over time

When you turn 55, a new Retirement Account (RA) is created. The money in your Special Account (SA) will be transferred to this, followed by funds in your Ordinary Account (OA).The amount transferred will be the Full Retirement Sum for the year, which is $198,800 in 2023.

Ms Lorna Tan, head of financial planning literacy at DBS Bank, says that by starting early, “it is possible to grow CPF balances to at least the Full Retirement Sum at age 55”, even if you start small because you have time on your side.

2. Add to your SA via the Retirement Sum Topping-up Scheme

You could transfer your OA savings to your SA, up to the Full Retirement Sum, before you turn 55 and so benefit from higher interest rates payable in that account, now at 4 per cent a year.You can also top up your SA with cash to the Full Retirement Sum and get a tax relief of up to $8,000 per calendar year.

Ms Tan says CPF members should do their top-ups at the beginning of the year, noting: “As CPF interest is calculated monthly, if a CPF member makes a top-up in January instead of December each year, he will earn 20 per cent more in interest over 10 years.”

CPF members who have turned 55 can also set aside more for retirement by transferring their OA and SA savings to their RA up to the Enhanced Retirement Sum, which is $298,200 in 2023.

You can also top up with cash to the Enhanced Retirement Sum, but you will not qualify for the $8,000 tax relief.

Tax relief applies only for cash top-ups to the Full Retirement Sum. Top-ups above this up to the Enhanced Retirement Sum of $298,200 this year will not qualify.

If you set aside only the Full Retirement Sum instead of topping up to the Enhanced Retirement Sum, you can just leave your remaining CPF money in your OA and SA, where it will continue to earn interest.

After you turn 55, the yearly increase in the Full Retirement Sum does not affect you any more. The Full Retirement Sum you need to set aside depends on when you turn 55 and is fixed for the rest of your life. However, you can continue to set aside up to the prevailing Enhanced Retirement Sum.

3. Make voluntary contributions to all three CPF accounts (Ordinary, Special and MediSave)

If you have topped up to your Full Retirement Sum (below 55) or Enhanced Retirement Sum (over 55), you can still put in more money under the CPF Voluntary Contribution Scheme.DBS’ Ms Tan says these top-ups go into Ordinary, Special and MediSave Accounts, up to $37,740, known as the CPF Annual Limit.

The maximum amount of voluntary contributions to the three CPF accounts is the difference between this annual limit and the amount of mandatory CPF contributions received for the year, Ms Tan adds.

Voluntary contributions do not enjoy tax relief, unlike cash top-ups under the Retirement Sum Topping-up Scheme.

Ms Tan says making voluntary contributions may be a great idea if you have excess cash that you do not need in the near term, but it may not work if you are in a tight financial situation and need money for more pressing things.

She adds that the CPF Voluntary Contribution Scheme is useful for senior members who have lower mandatory contributions as they grow older.

4. What if you cannot set aside the Full Retirement Sum?

Some CPF members fail to set aside the Full Retirement Sum for many reasons, such as having used funds to buy a house or because they stopped working to take care of children or an elderly parent.These members can set aside half of the Full Retirement Sum, which is the Basic Retirement Sum if they own a property. This Basic Retirement Sum is $99,400 in 2023.

Ms Tan says these members will have to restore their RA back to the Full Retirement Sum with the proceeds when they eventually sell their property.

She adds that there will be a second transfer of CPF savings to the RA, at the payout start age, which can be any time from age 65 to 70.

This applies to those born in 1958 or later, and who have not met their Full Retirement Sum by 55.

CPF members who have to stop working have options as well.

Ms Tay Mui Huang, senior adviser at Financial Alliance, says their spouses can transfer some of their CPF savings to their CPF accounts. Their spouses can also do a cash top-up for them up to the current Full Retirement Sum. These top-ups can bring tax relief of up to $8,000 a year.

5. CPF SA shielding as a way to grow CPF savings

DBS’ Ms Tan points to CPF SA shielding as a way to help members retain as much of the cash in their SA as possible, instead of the entire amount being swept into the RA.She adds that SA shielding should be done a few weeks before a member turns 55.

“Leave behind $40,000, which is the minimum amount that a member needs to keep in his SA. Invest the rest temporarily in a short-term and relatively safe investment product under the CPF Investment Scheme,” Ms Tan notes.

When the member turns 55, $40,000 from his SA and savings from his OA – up to the Full Retirement Sum – will be transferred to his RA.

“The CPF member can then liquidate his temporary investment, and the amount invested plus gains (if any) will return to his SA,” Ms Tan says.

This allows the CPF member to retain most of his SA savings, which will continue to earn interest at 4 per cent a year.

You can withdraw this interest earned regularly, effectively getting a “passive income stream to fund retirement needs”, Ms Tan notes.

The rest of the SA savings can stay in the CPF to compound and earn interest every year, she adds, likening this to a “fixed deposit with interest of 4 per cent per annum”.

But Ms Tan urges being careful when picking an investment product to park your SA savings temporarily. “If the fund value drops during the investment period, the CPF member may have to stomach losses on his SA savings, or he may consider liquidating it later.”

More people voluntarily contributing to retirement scheme amid uncertainties

4 myths that stop some from enjoying CPF’s benefits

6. If you meet your Full Retirement Sum, can you withdraw your remaining CPF savings?

You can withdraw at least $5,000 or any amount in excess of that after setting aside your Full Retirement Sum from the age of 55.You can withdraw this money at any time after 55, whether in full or partially.

The CPF Board notes: “If the member subsequently decides to put back the money in his CPF, he can do so by topping back up to the prevailing Enhanced Retirement Sum. This top-up will, however, not qualify for tax reliefs.”

Ms Tan adds that CPF members born in 1958 or later “can withdraw an additional amount of up to 20 per cent of their retirement savings at 65”.

However, you will not be able to withdraw cash top-ups or CPF transfers you have made to your retirement savings, she says, adding that you also cannot withdraw government grants to your CPF such as the CPF Life Bonus.

“CPF members will also need to be mindful that they are forgoing risk-free interest that they will otherwise earn if they leave the money in their CPF accounts,” Ms Tan adds.

Sperm bank ?Which bank in the world has enough money to give depositer back their money now ??

you must be out of your mind if you volunteer to put money in cpf .........

Similar threads

- Replies

- 5

- Views

- 1K

- Replies

- 0

- Views

- 369

- Replies

- 0

- Views

- 521